Why the Fed’s cautious about rate cuts

Despite geopolitical risks, strong fundamentals, steady earnings and persistent demand from retirement flows continue to support stocks

5 min read

KEY POINTS

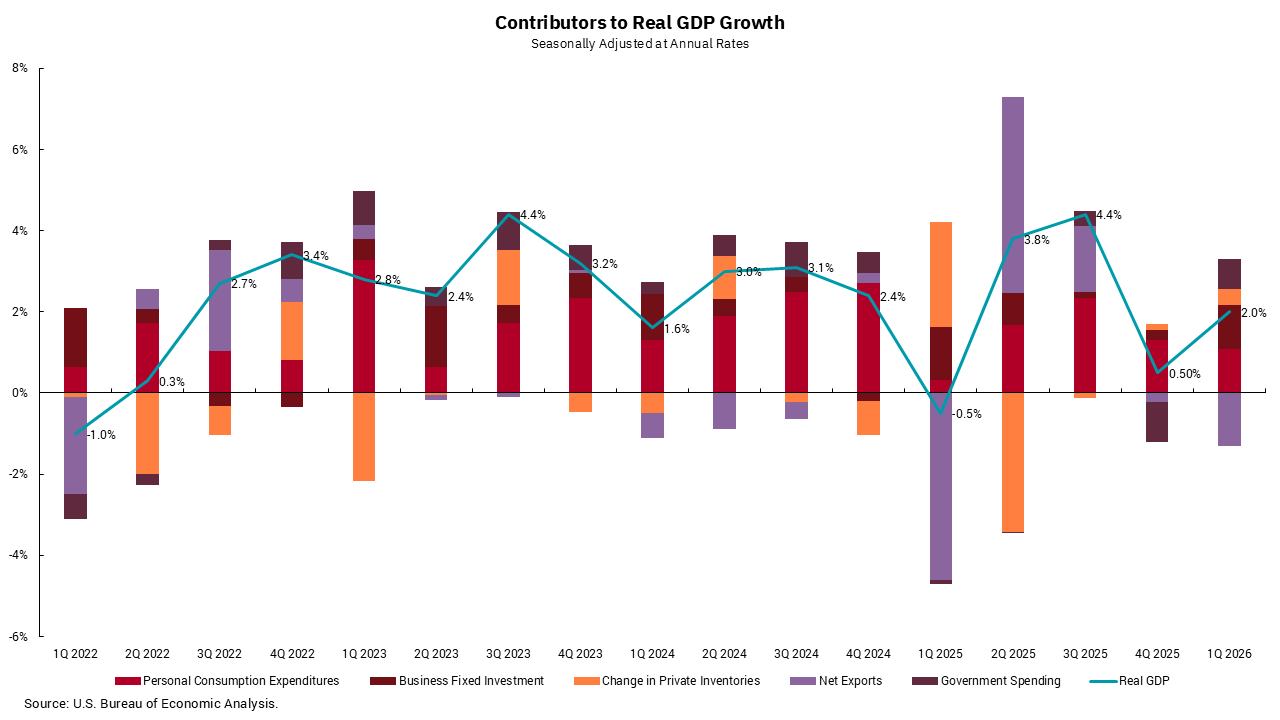

- The U.S. economy grew 2% in the first quarter of 2026, rebounding from shutdown driven weakness late last year and reinforcing its underlying resilience.

- Labor markets remain historically strong and business investment—led by an unprecedented AI capex cycle nearing 2% of GDP—is broadening economic support.

- Energy driven inflation tied to geopolitical conflict has pushed headline inflation higher, making near term interest rate cuts increasingly difficult despite stable core pressures.

The initial reading of first-quarter 2026 gross domestic product (GDP) is 2%, which shows that the economy reacted as anticipated. The U.S. entered the new year with growth moving higher from the shut-down depressed state it was in the fourth quarter of 2025, when the reading was only 0.5%. We know much of the impact of the Iran conflict remains ahead of us, but March’s numbers could have been impacted in this report.

As has been true for the last few quarters, the overall story of the U.S. economy is one of resilience. The. U.S. has taken quite a few shocks to the economy, yet the U.S. consumer has remained strong, the job market has remained supportive and, now, business investment looks to broaden beyond AI to additional sectors of the economy.

Speaking of the AI capex super-cycle, the total announced investments for 2026 have totaled about $600 billion so far. Given that U.S. GDP is around $30 trillion dollars, these announced investments represents 2% of GDP in AI capex. The last time we had a single part of our economy show similar levels of investment compared to GDP was in the 1870s when the railroads connected our country as never before. In addition to the huge investment, there were worries about the railroad’s impact on jobs, as there are today with AI. However, looking back, we now know that the railroad’s impact on the U.S. and its economy were materially positive. We feel similarly about the short-term versus long-term impacts on jobs from AI.

Speaking of jobs, weekly jobless claims, an important marker for us as we think about the health of the labor market, fell last week to 189,000, the lowest figure since 1969—and that’s without any adjustment based on the size of the labor force, which is much larger today. Continuing claims are slowly improving as well, so while hiring remains a bit slower, the evidence suggests that companies are retaining the vast majority of workers.

Within the GDP number, we also get some important readings on inflation. On this front, we can see the impact of the Iran conflict on energy prices and headline level inflation. The surge in energy prices led to a 0.7%-increase in inflation and year-over-year inflation increasing to 3.5%, from 2.8%. At the core level, however, the gains were more subdued as rents and wages remain constrained, which resulted in an increase of 0.3% and 3.2% year-over-year. We are watching the conflict in Iran closely from this perspective, as the longer the conflict continues, the greater the risk of higher energy prices for longer which will eventually lead to higher core inflation, too.

The change in chairmanship at the Fed notwithstanding, the coming impulse towards higher inflation will make the idea of interest rate cuts very difficult to consider. The vote to leave interest rates the same at the Fed’s April meeting was 11-1. The one dissenting vote was from recent President Trump-nominee Stephen Miran who wanted to see a 0.25% cut in rates. Miran’s consistent call for more and larger cuts than the consensus helps illustrate the potential risks the markets see to the change taking place at the Fed. The President has been clear in his thoughts to lower rates, so it is hard to imagine Kevin Warsh got the nod to be the next Fed Chair without some sort of at least ideological agreement on rates. The opposition to that idea was reflected in a push to remove the “easing bias” from the Fed’s statement, as well as in current Chair Jay Powell’s announcement he will stay in his seat as a board member after his term as chairman expires. This breaks with past protocol but Powell specifically pointed to the risk of politicizing the Fed as his reason for doing so. Fed watching is getting a bit more interesting.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)